ZKX Funding Rate: Adaptive Balancing Rate

TL;DR:

- Every exchange has its own funding rate, and ours is called Adaptive Balancing Rate.

- Our funding rate is based on Bollinger bands and takes into account the jumps of the underlying asset.

- The ABR provides a premium to assets with higher implied volatility and thus reducing risk exposure for the overall market.

Introduction

The Technical Paper is authored by Busra Temocin, Vitaly Yakovlev, Eduard Jubany Tur, and Naman Sehgal.

It covers the following aspects:

- Quantitative description of the ABR Mechanism and its dependency on Bollinger Bands

- Data Analysis of different exchange’s funding rates in relation to the jumps in the underlying assets price

- Calculation of Trading Spike windows under different funding rates

- How ABR responds under a Black Swan event and long-term profit and loss analysis.

Perps and Funding rate

Perpetuals, or perps, are financial instruments available on exchanges that differ in implementation. They function like spot trading instruments but are synthetic and allow for leverage. The term perpetual is significant because there is no expiration or settlement date.

Since perps have no expiration date, a funding rate is introduced to tie the price of the perp close to the price of the underlying asset.

Perp price > Index Price = > Funding rate positive – Long pays short

Perp price < Index Price = > Funding rate negative – Short pays long

If the majority of traders go short, the orderbook is unbalanced, and an incentive is required to restore balance in the orderbook on both sides. The trader's direction causes an imbalance in the depth of the market of the orderbook, and that's why incentives work to bring the perp price back in line with the spot price.

The ABR Mechanism

The ABR is calculated using Bollinger Bands, which are price envelopes drawn above and below the simple moving average of the price at a standard deviation level.

What is the role of the premium?

The ABR premium is a proxy of volatility of the underlying asset, measured through the Bollinger Band. When volatility rises, traders take more bets or leave the orderbook, creating additional risk. So, a premium is added to balance the risk, but it's removed when volatility decreases and traders go in either direction of the book.

We integrate the difference between Bollinger Band Price and Mark price. This difference is then added to the funding premium through logarithmic function.

The Price Differences are denoted by –

Du = Mark Price − Upper Band Value

Dd = Lower Band Value − Mark Price

At the end of every hour, we calculate the 1- hour premium using the time-weighted average price (TWAP). We look at the premiums from the past hour and come up with an average. A fixed interest rate is also added to account for the difference in interest rates between the base and quote currencies. This combined is known as the Funding rate.

The rate is charged/ paid to ZKX traders every 8 hours, in the initial implementation of the model. The rate will be adjustable in the long run.

Data Analysis

In this section, we have analyzed which exchange’s funding rate correlates most with the underlying asset. We have taken random sample data from dYdX, Deribit, and Binance between 05.11.22 and 03.01.23.

We have analyzed the data across three statistics: Mean, Standard Deviation and Correlation of the funding rate of the three exchanges

1. Descriptive statistics of different funding rate

-

The data indicate that the mean of ABR is second to largest and negative with a standard deviation that is rather small despite the jump dynamics.

-

Moreover, ABR has the highest correlation to BTC, indicating successful adherence to market behavior.

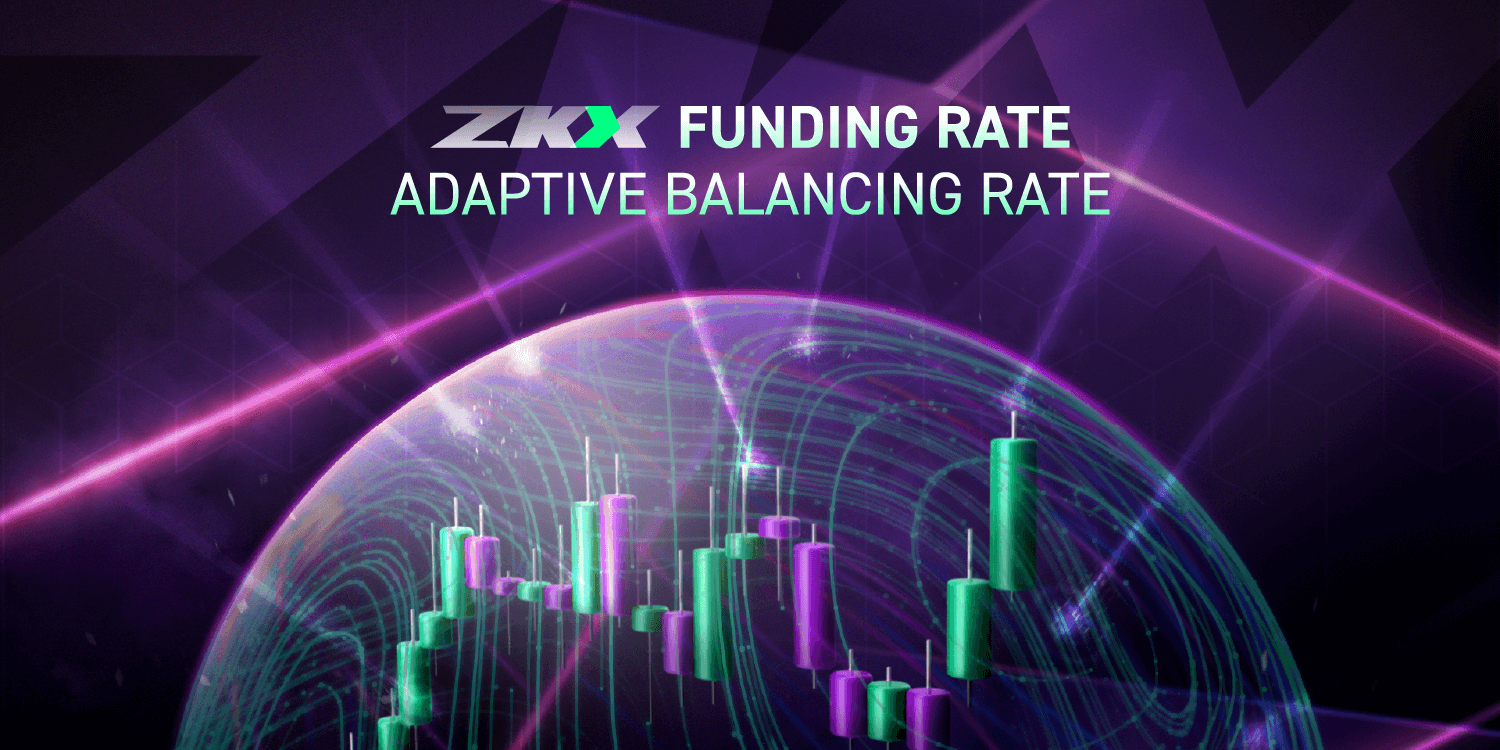

2. Comparison of funding rates (ZKX, dYdX, and Binance)

Here, the ABR is in line with the other counterparties and is evolving with a premium at times due to the loaded jump factors.

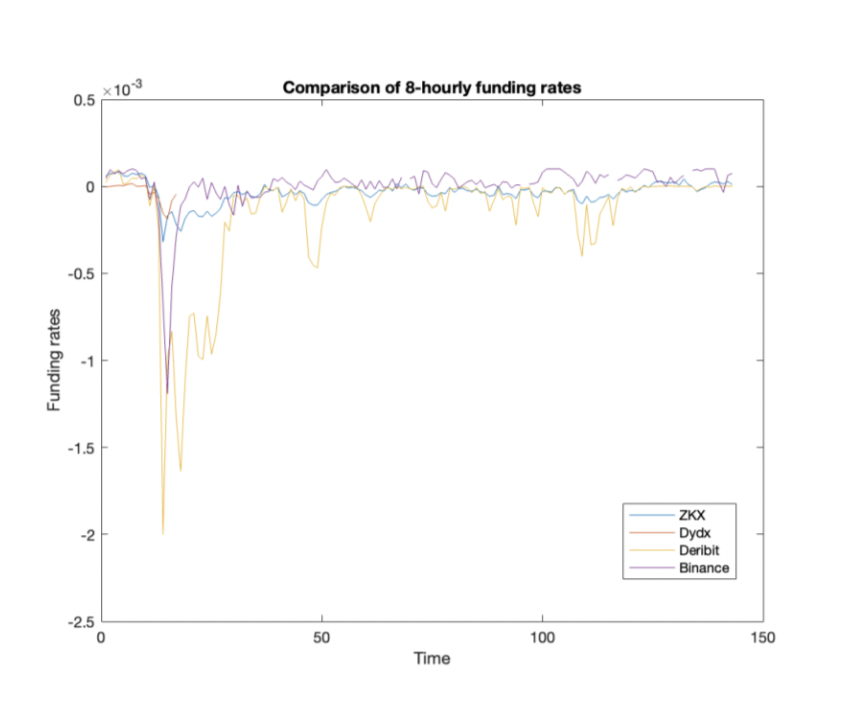

3. Comparison of 8 hourly funding rate averages across exchanges

Here the funding rate of the exchanges is shown every 8 hours. While there was a downward spike for all exchanges, ABR remained higher than others later on because of the jumps in the mark price and funding rate.

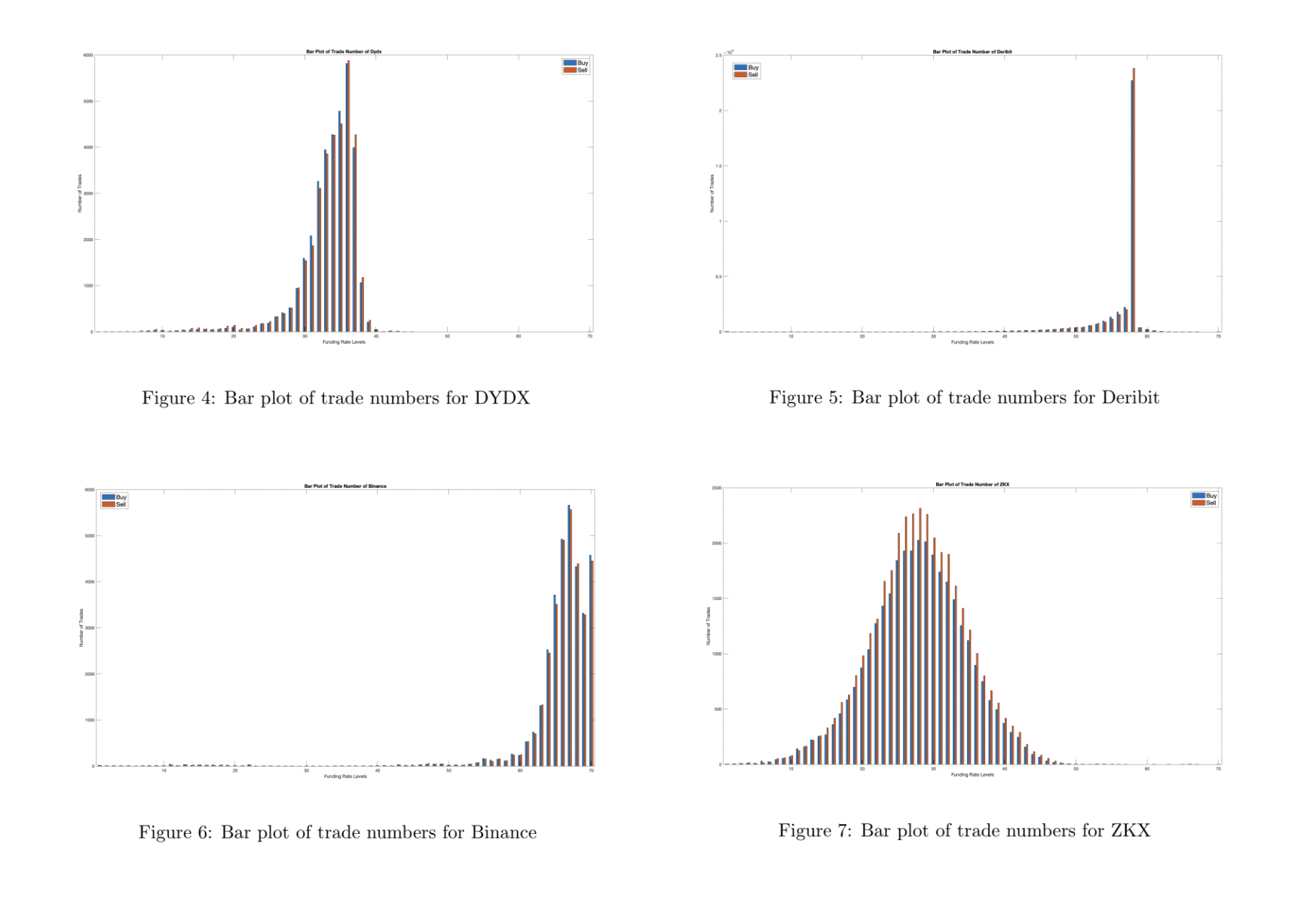

Trading Spikes

Trading Spikes examines the funding window of the most profitable exchanges, providing valuable insights for investors to gauge expected trading activity. Our analysis focuses on data samples from dYdX, Deribit, and Binance.

Figures 4, 5, and 6 depict various exchanges' trading frequency and magnitude, with spikes indicating the highest trading activity levels. As ZKX is yet to launch, we used a classification tree method to predict its trading frequency and magnitude, shown in Figure 7.

It has a wider window and higher frequency and magnitude than other exchanges, promising consistent trading opportunities.

To increase trading activity, exchanges should keep their funding rate within the range where the graphs show the maximum trading activity.

Black Swan Event

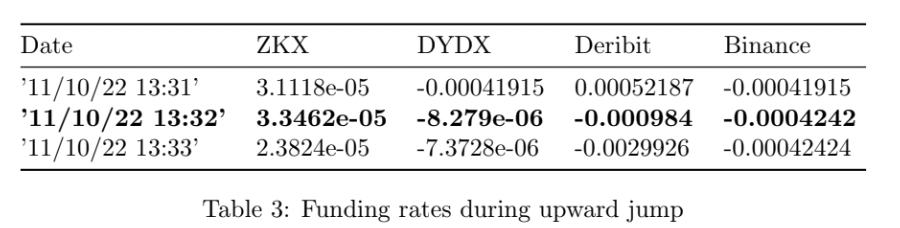

In this section, we are examining what happens during a black swan event, characterized by significant jumps in mark price and funding rate.

- The data shows that the largest upward jump in mark price happened on November 10th, 2022, at 1:32 pm, and it was a magnitude of 316.21$.

- Table 3 shows that ABR reacted efficiently to the significant jump, with a loading jump factor of 2.3440e-06.

- However, other exchanges, except for dYdX, did not respond to the jump similarly and instead had a lower change.

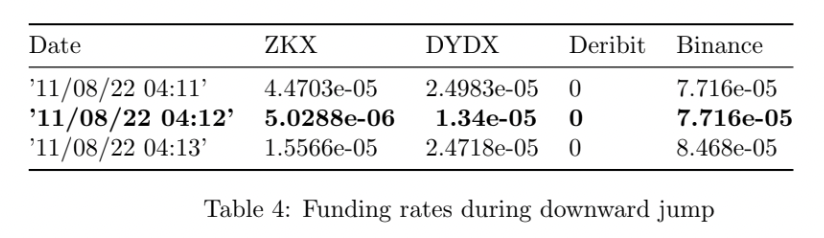

- The largest downward jump occurred on November 8th, 2022, at 4:12 am; it was 206.59$ in size. Table 4 indicates that only ZKX and dYdX were affected and experienced reduced rates during this sudden decrease in mark price.

- ABR's downward jump magnitude was 3.9674e-05, almost four times larger than dYdX.

- Given the strong reaction of ABR to unexpected price movements in the perpetual swap, one may question its long-term benefits and profit and loss performance.

The next section delves into this phenomenon.

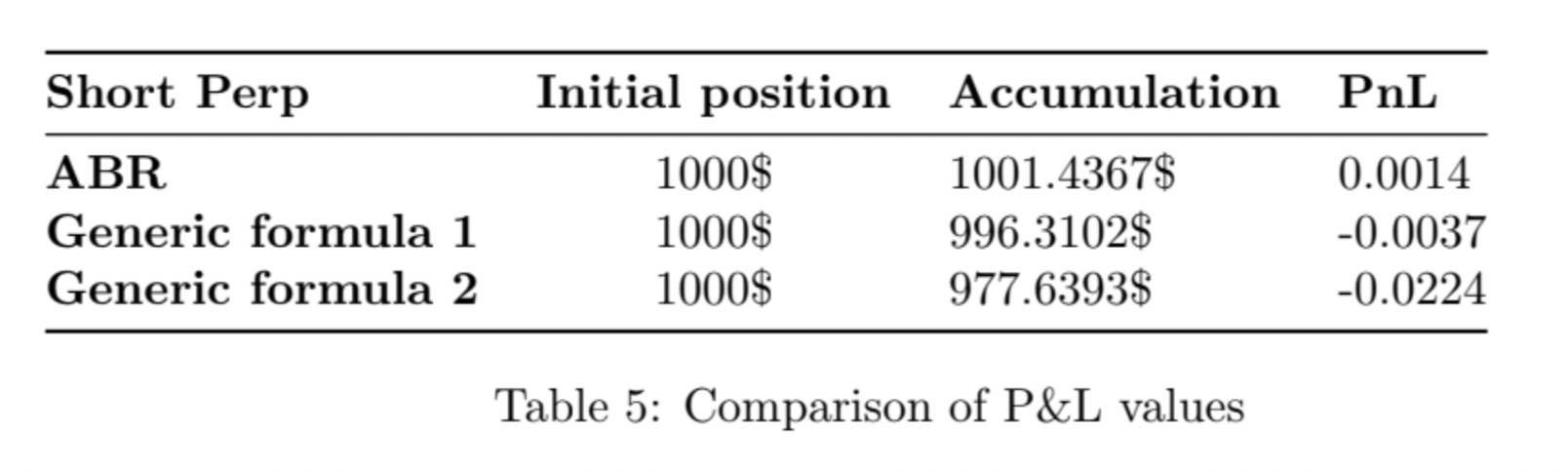

Profit and Loss

The current section compares ABR's methodology to existing generic funding rate formulas available in the market.

- Table 5 evaluates P&L values for 8-hourly funding, comparing ABR's funding rates to generic funding rate formulas in the market.

- The assessment involves holding an initial short position value of 1000$ and comparing accumulated funding payments over selected days.

- Results show that ABR's funding mechanism is the only one that generates a positive P&L compared to other counterparties.

Click here to read the Technical Paper.

About ZKX

ZKX is the first perpetual futures exchange on StarkNet with self custody and true community governance. The protocol is designed to provide further scalability with a decentralized node network, an elevated trading experience and offer perpetual swaps and derivatives to any user on Starknet and Ethereum. ZKX’s mission is to democratize access to global yields through its offerings to anyone, anywhere.

In July, ZKX raised $4.5m in seed funding from backers including StarkWare, Amber Group, Huobi, Crypto.com and others.